What is Microeconomics?

The term Micro has its origin in the Greek word called mikros which means small. Microeconomics studies the economic activities of an economic unit, like the demand for sugar by an individual household. It also studies the economic activities of a small group of economic units like the demand for sugar by all the households.

An Introduction to Microeconomics

Central Topic of Microeconomics

When economic problems such as unlimited wants, limited means, and alternative uses of limited resources are studied and addressed at the level of individuals, it is called microeconomics. The market forces such as demand and supply play an important role in addressing various microeconomic problems. This branch of economics assumes that macro variables remain constant. For example, when we are studying the determination of the price of an individual firm, it is assumed that the aggregate price level is constant.

Concepts Studied under Microeconomics

Microeconomics includes the study of the following concepts:

Utility theory: Utility refers to the satisfaction gained from the consumption of a good. This theory assumes that consumer purchase decisions are dependent on the degree of utility they derive from a product.

Demand theory: Demand refers to the desire of a consumer to buy a good and willingness to pay for the same. According to the law of demand, there is an inverse relationship between the quantity demanded and the price of the good while other things remain constant.

Demand Theory

Production theory: Production refers to combining various inputs to form output for consumption. Production theory studies the functional relationship between physical inputs and the physical output of a good.

Price determination: According to price theory, the price of a good or service is based on the relationship between its demand and supply. For example, prices should rise when the demand exceeds the supply and vice-versa.

Factor/Distribution pricing: There are four factors of production - land, labour, capital, and enterprise which are used for production purposes. The price that entrepreneurs pay for the services of these factors is known as factor pricing.

Microeconomics Question Bank with Answers

1. Explain the law of diminishing marginal utility?

Ans: Law of diminishing marginal utility states that as more and more units of a commodity are consumed by the consumer continuously, the marginal utility derived from every additional unit must decline. It is also known as the fundamental law of satisfaction.

2. What is the difference between the extension of demand and a decrease in demand?

Ans: When the quantity demanded increases due to a fall in the price of a commodity, it is known as the extension of demand. On the other hand, a decrease in demand occurs when the quantity demanded decreases due to factors other than the price of the commodity.

3. Explain the law of supply? Write about the effect of GST on the supply curve.

Ans: According to the law of supply, quantity supplied increases with an increase in the price of a good and vice-versa.

A rise in GST will raise the cost of production. This enables the producer to sell at a higher price. This is a situation of a decrease in supply or a backward shift in the supply curve.

4. Explain the law of variable proportions?

Ans: According to the law of variable proportions, as more and more of the variable factor is combined with the fixed factor, the marginal product of the variable factor may initially rise at an increasing rate. But eventually, a situation must come when the marginal product of the variable factor starts declining. It may also become zero or even negative.

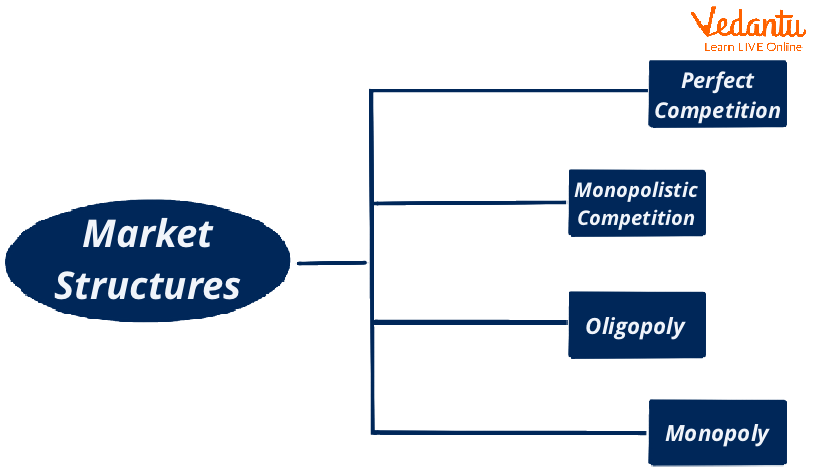

5. Explain the forms of the market.

Ans: The following are the principal forms of the market:

Perfect competition: When there are a large number of buyers and sellers of a commodity, and no individual buyer or seller has any control over the price of the commodity, it is said to be perfect competition.

Monopoly: Monopoly is a situation in the market where there is only a single seller of a product with no close substitutes in the market.

Monopolistic competition: It is that form of market where there are many buyers and sellers of the product, but the product of each seller is different from another.

Oligopoly: It is that form of market where there are a few big firms and a large number of buyers of the product. The price and output decisions of one firm impact the decisions of other firms in the market.

Conclusion

In a nutshell, microeconomics is related to supply and demand factors in the economic environment. It helps design various economic policies. Moreover, microeconomic theories help in the efficient utilisation of scarce resources to carry out production processes efficiently. Microeconomics principles also guide better decision-making. It helps the businessmen in making various decisions to maximise profit. It is also important for the economic development and growth of the country. Microeconomics also studies human behaviour. The law of diminishing utility and indifference curve theory both study human behaviour.

FAQs on Microeconomics: A Detailed Overview

1. What is microeconomics and what are its main components?

Microeconomics is the branch of economics that studies the behaviour of individual economic units, such as households, firms, and industries, and their interactions in markets. It focuses on how these units make decisions regarding the allocation of scarce resources. The main components of microeconomics include the Theory of Consumer Behaviour, the Theory of Producer Behaviour, and the Theory of Price.

2. What is the scope of microeconomics?

The scope of microeconomics is wide and covers the study of several key economic theories. Its primary areas of focus include:

- Demand Theory: Analysing consumer behaviour and demand patterns.

- Production Theory: Studying the relationship between inputs and outputs in a firm.

- Price Determination: Understanding how prices for goods and services are set based on demand and supply forces.

- Factor Pricing: Determining the rewards for factors of production, such as wages for labour, rent for land, and interest for capital.

3. What are the central economic problems that microeconomics addresses?

Microeconomics addresses the fundamental economic problems of scarcity and choice at an individual level. It provides a framework to understand:

- What to produce: Which goods and services should be produced with limited resources.

- How to produce: Which combination of factors or technology should be used for production.

- For whom to produce: How the produced goods and services should be distributed among the population.

4. How does microeconomics differ from macroeconomics?

The primary difference lies in their scale of study. Microeconomics focuses on individual economic agents like a single consumer or a single firm, analysing individual prices, demand, and supply. In contrast, macroeconomics studies the economy as a whole, dealing with aggregates like national income, inflation, unemployment, and overall price levels. A simple analogy is that microeconomics studies the individual trees, while macroeconomics studies the entire forest.

5. How can principles of microeconomics be applied in real-life decision-making?

Microeconomic principles are constantly used in everyday life. For example, when you decide how to spend your pocket money, you are using the concept of opportunity cost and utility maximisation. Similarly, a local shopkeeper uses the principles of demand and supply to set the price for their products. Businesses also use microeconomics to make decisions about production levels, pricing strategies, and hiring employees to maximise profits.

6. What are the different types of market structures studied in microeconomics?

Microeconomics analyses how firms behave in different market structures. The main types are:

- Perfect Competition: A market with a large number of buyers and sellers dealing in a homogeneous product.

- Monopoly: A market with a single seller who has complete control over the supply of a product with no close substitutes.

- Monopolistic Competition: A market with many sellers offering differentiated products, blending elements of monopoly and competition.

- Oligopoly: A market dominated by a few large firms whose pricing and output decisions are interdependent.

7. Why is microeconomics often called 'Price Theory'?

Microeconomics is often referred to as 'Price Theory' because its central subject matter is the determination of prices in the market. It explains how the interaction of the forces of demand and supply determines the price of a particular commodity and the prices of factors of production (like wages, rent, and interest). Almost every major theory within microeconomics, from consumer behaviour to market structures, ultimately contributes to understanding this price-setting mechanism.

8. What are the main limitations of microeconomic analysis?

While useful, microeconomics has certain limitations:

- Unrealistic Assumptions: Many microeconomic models are based on simplifying assumptions like 'ceteris paribus' (all other things being equal) and the existence of perfect competition, which may not hold true in the real world.

- Focus on a Small Part of the Economy: It examines individual units in isolation, which can lead to the 'fallacy of composition'—what is true for an individual may not be true for the entire economy.

- Ignores Macroeconomic Factors: It does not analyse the impact of crucial macroeconomic variables like national income, employment levels, or government policies on individual economic behaviour.